EIA Report - More Oil Wells Completed

|

Petroleum & Other Liquids

Number of drilled but uncompleted wells declines

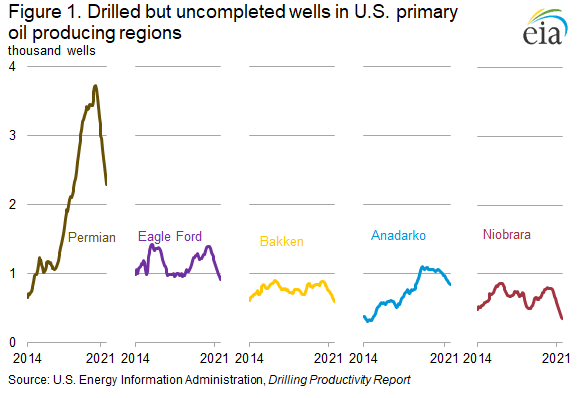

Based on our latest Drilling Productivity Report (DPR), there were 5,957 drilled but uncompleted wells (DUCs) in all DPR regions in July 2021, the fewest in any month since November 2017 (Figure 1). The decline in DUCs in most major U.S. onshore oil producing regions, most notably the Permian region, reflects an increase in well completions while new well drilling activity remains low. The combination of more wells being completed but fewer wells being drilled is contributing to the return of oil production in the Permian region; however, it is driving the current DUC inventories down, which could limit oil production growth in the United States in the coming months.

The two main stages in bringing a horizontally drilled, hydraulically fractured well online are drilling and completion. The drilling phase involves dispatching a drilling rig and crew, who then drill one or more wells on a pad site. The next phase, well completion, is typically performed by a separate crew and involves casing, cementing, perforating, and hydraulically fracturing the well for production. In general, the time between drilling and completion stages takes several months, leading to a natural buildup of DUCs, which producers can maintain as a set of working inventory to manage oil production.

Of the five major U.S. oil producing regions, DUCs in the Eagle Ford, Bakken, and Niobrara have declined to the lowest level on record since December 2013, and DUCs in the Permian and Anadarko regions have declined to the lowest level since June 2018. Although the significant reduction in DUCs follows an increasing rate of well completions in the Permian region, both the number of wells drilled and completed in all other regions remain at historically low levels (Figure 2).

Given that fewer new wells have been drilled than have been completed in recent months, DUC inventories may continue to decline. Based on our latest DPR, 393 wells were completed in the Permian region in July 2021. At that monthly completion rate, the Permian region has less than six months of DUCs remaining, which is approaching the lowest number of months of DUC inventory since September 2018. The low months of inventory in the Permian region may affect completion activity (slowing it down) or new well drilling activity (speeding it up).

The length of time between the drilling and completion phases affects the total time it takes to complete a well. Limited crew availability and delayed delivery of equipment and materials can stretch the time required to complete a well from a few days to more than a year. The drilling and production process of an oil well starts with the initial drilling, or spudding. Since 2014, the average spud-to-completion time has increased in most major oil producing basins in the United States. Technological complexity, including longer horizontally drilled wells during the drilling phase and multistage fracturing during the completion phase, has increased since 2014 and has contributed to longer spud-to-completion times. In addition, the number of wells that crews simultaneously work on in the completion phase has increased, and trade press cites operators claiming a number of higher efficiencies by completing multiple wells simultaneously. Monthly FracFocus data indicate that an average frack crew in 2021 now works on completing an average of about 2.5 wells at the same time, up from 1.8 wells in 2017 and about 1.6 wells from 2014 to 2017 (Figure 3). Based on data from FracFocus, we estimate the most likely spud-to-completion time for all U.S. oil producing basins in 2019 was 3.0 months, up from 1.7 months in 2014. In 2020, the impacts of the COVID-19 pandemic led to a sharp decrease in both drilling and completion activities, and the most likely spud-to-completion time increased to 3.5 months. As of the latest completion data available for 2021, the most likely spud-to-completion time increased to 4.2 months.

Indicators of new well drilling in the United States remain subdued. As of August 20, the Baker Hughes active oil rig count was 405 rigs. Although representing an annual increase of 222 rigs, this rig count is historically low compared with other periods when front-month crude oil futures prices were near similar levels or at even lower prices (Figure 4). Increases to rig counts typically lag four to six months behind a price increase. If drilling activity doesn’t increase, then well completions and production may be limited as the inventory of DUCs continues to fall.

U.S. average regular gasoline and diesel prices decrease

The U.S. average regular gasoline retail price decreased nearly 3 cents to $3.15 per gallon on August 23, 96 cents higher than the same time last year. The Midwest price decreased nearly 6 cents to $3.00 per gallon, the Gulf Coast price decreased more than 4 cents to $2.80 per gallon, the East Coast price decreased nearly 2 cents to $3.02 per gallon, the West Coast price decreased more than 1 cent to $3.95 per gallon, and the Rocky Mountain price decreased nearly 1 cent to $3.66 per gallon.

The U.S. average diesel fuel price decreased more than 3 cents to $3.32 per gallon on August 23, 90 cents higher than a year ago. The Midwest price decreased more than 4 cents to $3.22 per gallon, the West Coast and Gulf Coast prices each decreased nearly 4 cents to $3.99 per gallon and $3.04 per gallon, respectively, and the East Coast and Rocky Mountain prices each decreased by nearly 2 cents to $3.30 per gallon and $3.64 per gallon, respectively.

Propane/propylene inventories rise

U.S. propane/propylene stocks increased by 2.0 million barrels last week to 68.7 million barrels as of August 20, 2021, 14.5 million barrels (17.4%) less than the five-year (2016-2020) average inventory levels for this same time of year. Midwest, East Coast, Gulf Coast, and Rocky Mountain/West Coast inventories increased by 0.8 million barrels, 0.6 million barrels, 0.3 million barrels, and 0.2 million barrels, respectively.